.svg)

Article by Julie Gilson, Business Analyst at Gambit. When we launched Birdee - our B2C robo-advisor- in 2017, one of our main goals was to get market insights first-hand from our customers. With the feedback and insights of real users, we are able to build better solutions and offer live-tested technology to our B2B customers. In a series of articles, we focus on some interesting statistics that could help other companies when starting an online advisory service.

This week: Do people follow the advice given by an algorithm?

Like many robo-advisors, Birdee targets a retail to mass-affluent client-base, that is not necessarily familiar or comfortable with financial subjects. Therefore, robo-advisors typically guide the customer towards a suitable investment portfolio based on an interactive questionnaire. This advice is grounded on critical information like financial objectives, time horizon, risk aversion and financial situation. But do customers follow this recommendation, or do they opt for a different portfolio in the end?

How is advice given?

During the on-boarding and subscription, our clients are asked to answer several questions in order to evaluate their individual’s willingness to take risks and better identify their needs. The questionnaire is made up of interactive multiple-choice questions. These include a hypothetical choice between different market returns (positive and negative) and the customer’s reaction to sudden market turbulence. All of this is made as interactive and visual as possible.

Example of a visual question in Birdee

Example of a visual question in Birdee

Based on this, an algorithm determines the suitable risk profile for the customer. A coherency check is performed in order to ensure that the answers provided are consistent with previously provided information.

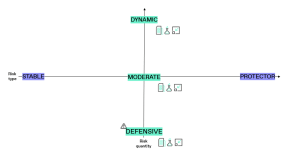

A particularity to Birdee, is that the algorithm goes beyond the typical risk-aversion assessment, but proposes 5 different risk profiles over two axis: risk aversion and risk perception.

Birdee’s 5 risk profiles

Once the risk profile is determined, Birdee suggests a suitable investment portfolio. Birdee takes an advisory role but its recommendation is not compulsory. The user is free to choose another portfolio (even one that does not fit his/her risk profile). Of course, the necessary warnings are in place in case a customer deviates from this advice.

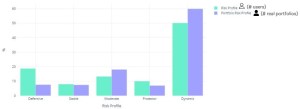

Dynamic profiles are the majority

Looking at the data of real investors and people with virtual portfolios, Birdee clearly attracts predominantly dynamic investors. Indeed, the dynamic offer accounts for about 50 percent of Birdee’s customer base.

Distribution of the different risk profiles

Distribution of the different risk profiles

This conclusion is valid for both genders, independently of the age of the customer.

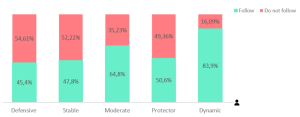

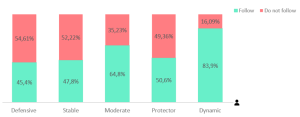

2/3 of the investors follow the advice

Although a suitable risk profile is proposed, a customer has the freedom alter this advice by choosing another a portfolio with different risk characteristics. We found it important to find a balance between reliable advice and freedom of choice. Therefore, we leave the final decision to the customer.

Although a large majority of customers follow the recommendation, a cynic might judge that almost 1/3 (27,9%) of Birdee investors decided not to follow the advice.

Defensive customers act differently

Interestingly enough, the rate at which people follow advice is not equal for all risk profiles. The dynamic recommendation is the most followed (83%). However, for the more defensive portfolios, personal preferences tend to diverge more frequently.

Almost 55% of the defensive risk profiles, chose a riskier profile than proposed. In the same line, the stable (28%) and moderate (21%) change their recommendation towards a riskier profile.

What could explain this statistic?

A first reflection might be that there is something wrong with the algorithm. Defensive and Dynamic risk profiles are relative concepts. A dynamic portfolio from one bank can be comparatively more moderate at another. Therefore, the definition of a risk profile should always be linked to the expected market behaviour or the portfolios.

This is exactly what Birdee does: the expected losses and gains are based on the real risk of the underlying portfolios. We are therefore convinced that there is nothing wrong with the calculation.

Birdee attracts predominantly dynamic investors. The dynamic offer accounts for about 50% of Birdee’s customer base.

A risk profile is personal, but also local

A more plausible explanation is that people assess their personal situation before they invest real money.

Losses and gains of an investment are almost always represented in relative terms (percentages) of the invested amount. But of course, this invested amount compared to the total wealth of the portfolio is an important criterion.

As an example: when a wealthy customer invests 1.000 euro, he/she is very likely to be less affected by a 10% loss than a less wealthy customer who invests 50.000 euro. Even if both investors have the same risk profile, the 10% loss is not equal for both.

Birdee has today no view on the total wealth of the customer and thus no way to judge how much the invested amount represents compared to the overall wealth.

The investment decision at Birdee, i.e. putting real money on the table, comes after the determination of the risk profile, and often after weeks of testing the platform with virtual money. This split in the journey is a thought-out choice, allowing the user to get familiar with the service and the risks linked to investments.

By the time that the customer is ready to invest, he / she has a very good idea of how much money he /she is ready to invest. This is then put into balance with the risk taken compared to the overall wealth. Since the first amounts invested are often relatively small, customers are ready to take more risk than their overall profile seems to indicate.

Almost 55% of the defensive risk profiles, chose a riskier profile than proposed. In the same line, the stable (28%) and moderate (21%).

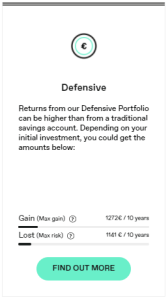

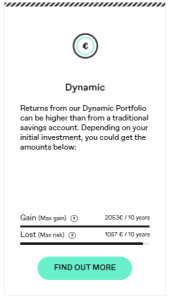

Visual elements in the customer journey also guide the user’s choice. When selecting a portfolio, Birdee projects the potential gain and loss of that profile. The customer can easily judge whether this risk is justified compared to the amount he or she is ready to invest.

Example of a risk/return comparison in Birdee

Robo advisors could become, but are not yet, financial planners

This brings us to the current role of a robo-advisor. Birdee is – like many robo-advisors- an efficient, low-cost and easy-to-use platform for investing money in a secure way.

However, the bridge towards a global advice on the wealth of the customer, based on all assets has not yet been made.

Technologically this is perfectly possible, since a lot of banks use the same technology as Birdee to provide a global wealth advice, but often with a financial advisor in the driving seat. It is only a matter of time before an online service starts incorporating this more global advice into its service.

Conclusion

Today, robo-advisors seem to seduce mainly investors with a dynamic risk profile, or at least people who wish to invest part of their money in risky assets. Although the advice provided by our robo-advisor is followed by 2/3 of the customers, especially defensively profiled customers select a more risky profile once they decide to invest real money.

This can be largely explained by the fact that the first steps people take with a robo-advisor are often low amounts, and that they are willing to take more risk if the amount is a fraction of their global wealth. This is perfectly fine, as long as customers are well informed, and able to re-evaluate this decision once the portfolio starts growing.

In the future, we can expect online advisory service to expand their scope and start integrating a more global, aggregated view of the customers financial situation. This technological evolution will enable robo-advisors to get a step closer to a comprehensive financial assistant.